If you are struggling to make your mortgage payment, you are not alone — and you have more options than you may realise. Search interest in “help with mortgage” has hit the highest level ever recorded in the United States, surpassing even the 2008 housing crisis. The good news is that lenders have more hardship programs available today than at any point in history. Acting early is the single most important thing you can do.

The key rule: call your servicer before you miss a payment. Once you are 30 days late, your credit score can drop 50–100+ points and your options narrow. Most of the programs below are available to borrowers who are current but expect difficulty — not just those already behind.

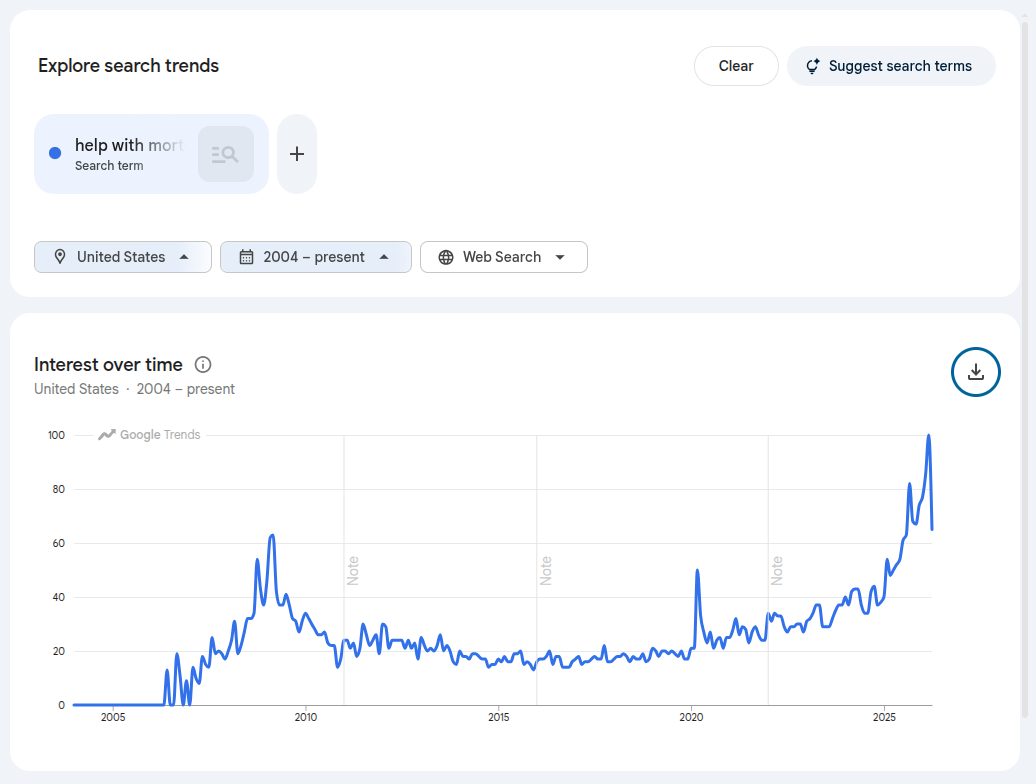

Why “Help With Mortgage” Searches Are at a Record High

Google Trends data shows that searches for “help with mortgage” in the United States have surpassed the previous all-time peak set during the 2008 housing crisis — a level that was, at the time, considered a once-in-a-generation event.

Source: Google Trends, United States, 2004–present. Interest score of 100 represents peak search interest.

The 2026 spike reflects a combination of factors: mortgage rates that remain elevated after two years above 6%, home prices that have not corrected, and an increasing number of homeowners who locked in adjustable-rate mortgages or interest-only terms that are now resetting to higher payments. If you are searching for help, the options below are where to start.

Option 1: Call Your Servicer and Request Forbearance

Forbearance is the fastest short-term relief available. Your mortgage servicer can temporarily pause or reduce your monthly payment — typically for 3 to 12 months — while you get back on your feet.

How it works:

- Contact your servicer (the company you send payments to) directly

- Explain your hardship — job loss, medical expense, income reduction

- Servicers are legally required under the Homeowners Protection Act to discuss loss mitigation options with you

- Approved forbearance pauses late fees and halts foreclosure proceedings

What you owe afterward: The skipped payments do not disappear. At the end of forbearance, your servicer must offer a repayment plan. The most common options are a lump-sum repayment, a repayment plan spread over future months, or tacking the amount onto the end of your loan.

For example: if you are paying $2,000/month and receive 3 months of forbearance, you would owe an extra $6,000 — typically either added to your last payments or spread over 12 months at ~$500 extra per month.

Option 2: Apply for a Loan Modification

A loan modification permanently changes the terms of your mortgage to reduce your monthly payment. Unlike forbearance, this is a long-term fix.

What servicers can change:

- Lower your interest rate (sometimes significantly)

- Extend your loan term (e.g., restart a 30-year clock to reduce monthly payment)

- Convert an adjustable rate to a fixed rate

- In limited cases, defer or reduce principal

How to apply: Contact your servicer’s loss mitigation department directly. You will typically need to submit a hardship letter, two recent pay stubs or proof of income, bank statements, and a recent tax return.

Modifications generally take 30–90 days to process. Continue making whatever payments you can during this time.

Option 3: Refinance to a Lower Rate

If you have equity in your home and your credit is intact, refinancing can permanently lower your payment without a hardship process.

A homeowner with a $400,000 balance at 7.5% pays approximately $2,797/month in principal and interest. Refinancing to 6.5% would reduce that payment to around $2,528/month — saving roughly $269/month.

Refinancing makes sense if:

- Current rates are meaningfully lower than your existing rate

- You plan to stay in the home long enough to recoup closing costs (typically 2–3 years)

- Your credit score is 620+ and you have 5–20% equity

Use the mortgage refinance calculator to see if the numbers work in your situation. Closing costs typically run $3,000–$7,000, so the math must work before you proceed.

Option 4: Access the Homeowner Assistance Fund (HAF)

The Homeowner Assistance Fund is a federal program administered by state housing agencies. Congress allocated $9.96 billion in HAF funds to help homeowners impacted by financial hardship.

HAF can pay for:

- Mortgage arrears (past-due payments)

- Property taxes in delinquency

- Homeowner’s insurance

- HOA fees

- Utility bills threatening habitability

How to apply: Find your state’s HAF program at consumerfinance.gov/haf. Funding availability varies — some states have exhausted funds while others still have active programs. Apply as soon as possible if you are eligible.

Option 5: Talk to a HUD-Approved Housing Counselor (Free)

The US Department of Housing and Urban Development (HUD) certifies nonprofit housing counseling agencies across the country. Their services are free and independent — they work for you, not the lender.

A HUD counselor can:

- Review your complete financial situation

- Negotiate directly with your servicer on your behalf

- Help you understand and apply for forbearance, modification, or HAF funds

- Advise on whether keeping the home is financially viable

Find a counselor: Call the HUD hotline at 1-800-569-4287 or search online at hud.gov/counselors. Counselors are available in every state.

Beware of for-profit “mortgage relief” companies that charge upfront fees to do what HUD counselors do for free.

Option 6: Rent Out a Portion of Your Home

If your home has a spare room or a rentable accessory dwelling unit, rental income can offset your monthly mortgage payment meaningfully.

The national median asking rent for a single room in a shared house was approximately $1,000–$1,400/month in 2026, depending on location. On a $2,000/month mortgage, a single room rental could cover 50–70% of your payment — potentially enough to stay current without any lender involvement.

Check local zoning laws and your mortgage documents. Most conventional mortgages allow owner-occupied rentals; FHA loans require owner occupancy but do not prohibit renting a room.

Option 7: Short Sale or Deed-in-Lieu of Foreclosure

If keeping the home is no longer financially viable, these two options allow you to exit without the full damage of foreclosure.

Short sale: You sell the home for less than the outstanding mortgage balance, and the lender agrees to accept the proceeds as full or partial settlement of the debt. A short sale typically damages your credit less than a foreclosure and allows you to buy again sooner (usually 2–4 years vs. 7 years for foreclosure).

Deed-in-lieu: You voluntarily transfer ownership of the property to the lender in exchange for being released from the mortgage debt. This avoids the foreclosure process entirely and is generally faster.

Both options require lender approval and will affect your credit, but neither as severely as a completed foreclosure. Talk to a HUD counselor before pursuing either option to make sure you have exhausted all alternatives.

Option 8: Know the Foreclosure Timeline — You Have More Time Than You Think

Many homeowners facing hardship do nothing because they fear immediate foreclosure. The reality is that federal law provides substantial protection:

| Stage | Timing |

|---|---|

| First missed payment | 15-day grace period in most loans before late fee applies |

| 30 days late | Reported to credit bureaus; servicer must contact you about options |

| 120 days late | Earliest legal point for servicer to begin foreclosure process |

| Foreclosure filing | Formal process begins; timeline varies 6 months–3 years by state |

| Sheriff sale / auction | Final stage of foreclosure — home transferred to new owner |

Federal law requires servicers to wait 120 days before initiating foreclosure, and they must inform you of loss mitigation options before filing. Even after a foreclosure notice is filed, you can often stop the process by entering forbearance, submitting a modification application, or selling the home.

What to Do Right Now — Step by Step

- Locate your servicer’s contact number. This is on your monthly statement or the servicer’s website — not the original lender if your loan was sold.

- Call before you miss a payment. Every day of lead time increases your options.

- Ask specifically for the loss mitigation department. This is the team that handles hardship programs — not general customer service.

- Document everything. Get the name of every person you speak to, the date, and what was agreed. Follow up in writing by email or certified letter.

- Contact a HUD counselor if the servicer is unresponsive or you need independent help.

If you are also dealing with what happens after missing payments — late fees, credit reporting, or the early foreclosure timeline — read the full guide on that process. For broader housing affordability context, see the mortgage affordability gap data and the ongoing average mortgage payment figures.

Summary: Mortgage Help Options at a Glance

| Option | Best for | Speed | Credit impact |

|---|---|---|---|

| Forbearance | Short-term hardship (job loss, medical) | Fast — days | None if approved before missing payments |

| Loan modification | Ongoing payment unaffordability | Slow — 30–90 days | None once approved |

| Refinance | Good credit, have equity | Moderate — 30–45 days | Small, temporary dip |

| HAF funds | Mortgage arrears, taxes, insurance | Varies by state | None |

| HUD counseling | Need guidance and negotiation help | Immediate | None |

| Room rental | Spare space available | Immediate | None |

| Short sale | Home underwater, can’t afford to stay | Moderate | Significant but less than foreclosure |

| Deed-in-lieu | No other options; want clean exit | Moderate | Significant but less than foreclosure |

The most important step is the first one: call your servicer today, before a payment is missed. The options available at day zero are far better than those available at day 90.

The content on Wealthvieu is for informational purposes only and should not be considered financial, tax, or investment advice. Consult a qualified professional before making financial decisions. Full disclaimer · Editorial policy